What Do Circle and Tether’s Proprietary Blockchains Mean for Ethereum?

GM,

The podcast will be on pause tomorrow. Let’s get into today’s topic. The ETHA (iShares Ethereum Trust ETF), launched by BlackRock, the world’s largest asset manager, is now the world’s largest Ethereum ETF by market capitalization. Over the past 75 trading days, ETHA has seen a cumulative net inflow of $8 billion, with net outflows on only 4 days. On August 11 alone, it attracted a record $1.01 billion in a single day. In comparison, the largest single-day net inflow for a Bitcoin ETF has been $178 million.

Wall Street institutions are buying ETH at a near-manic pace! The reason: they believe Ethereum will become the global settlement layer for stablecoins, and most stablecoins already run on Ethereum. More and more people are convinced that investing in ETH is essentially a bet that stablecoins will form the foundation of future financial infrastructure.

It’s a compelling narrative—but recently, doubts have begun to surface. Both of the world’s largest stablecoin issuers, Tether and Circle, have announced plans to launch their own blockchains, pulling USDT and USDC back “home.” Tether has even rolled out a subsidy strategy, promising that all USDT transfers on its own chain will be entirely gas-free.

Some online commentators argue this could “break the narrative that stablecoins drive ETH price growth.” If stablecoins migrate away from Ethereum, will Wall Street still need to buy ETH? Looking back at the history of technology, a similar drama already played out 30 years ago. In this article, I’ll use the history of the internet to explain why I believe stablecoin issuers building their own blockchains will, in the long run, only make Ethereum more valuable.

Internet Cafés

Readers around my age probably remember playing Counter-Strike (CS). This classic first-person shooter could be played solo, but the real fun was heading to an internet café with friends to battle it out!

Why didn’t we just play at home? Because internet cafés were faster. Back then, most people were still using dial-up connections, and the Internet simply couldn’t handle the split-second demands of a shooting game. Just a few milliseconds of lag could mean the difference between life and death. At an internet café, you could connect through a local area network (LAN), which wasn’t limited by the Internet’s speed. It wasn’t until broadband became widely available that people could enjoy stable connections at home, and internet cafés slowly disappeared.

Thirty years ago, many companies also believed that an “Intranet” was far more practical than the Internet. Intranets offered faster speeds and protection against outside hackers, making them safer and seemingly better suited for business needs. National Chengchi University recorded this history as follows:

Thanks to the “external connectivity” benefits of the Internet, enterprises could not ignore its power. But the open nature of the Internet conflicted with corporations’ need for closed systems—for example, concerns over information leaks or integration with existing infrastructure. Thus, the Intranet was born… The biggest difference was that the Intranet targeted a company’s internal information architecture, serving employees with the goal of strengthening communication and boosting efficiency.

At that time, the Internet was slow, email was flooded with viruses and spam, and it distracted employees at work. As a result, most companies restricted access to the “external web,” running email, collaboration tools, and file management services entirely on their own “intranets.” Years later, intranets still exist—but only in work settings. Today, nearly everyone’s digital life is built on the very Internet once dismissed as inefficient and risky. Why?

Tim Berners-Lee, the inventor of the World Wide Web (WWW), observed the rise of intranets in 1996 and argued that the openness of the Internet was the key to its success. Speed and security, he said, could improve with technological progress, but openness could not. Time proved him right. While intranets gave businesses short-term gains in speed and security, they limited their long-term potential. Today, the “external web” is the one everyone uses.

With this context in mind, we can better understand the true significance of Tether and Circle’s recent moves to launch their own blockchains.

Emergency Alliance Chains

The blockchains launched by stablecoin issuers are like the intranets that businesses once favored—products designed to solve immediate problems. Public blockchains like Ethereum, on the other hand, are the equivalent of the Internet for everyday life—built as century-long infrastructure. To confuse the two is like comparing chicken drumsticks to thighs: similar in appearance, but fundamentally different.

Tether’s Stable is marketed as a blockchain purpose-built for financial transactions, using USDT as its gas token and highlighting its efficiency in cross-border payments and transfers. Circle’s Arc is similar: it emphasizes paying gas fees in USDC, comes with built-in foreign exchange features, and aims to migrate the stablecoin ecosystem onto a chain it fully controls.

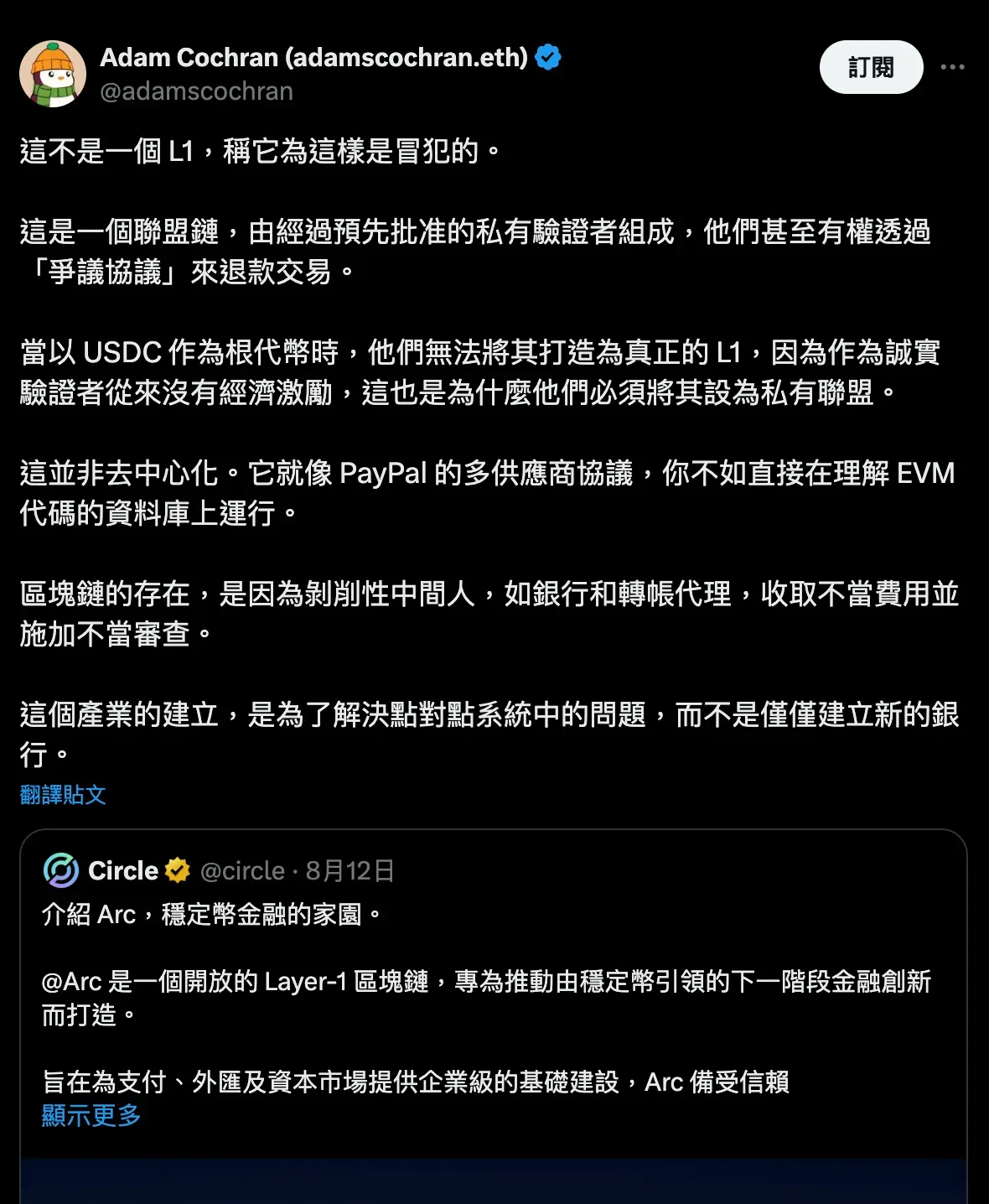

Although both brands promote their systems as Layer 1 blockchains, in reality their architectures are closed consortium chains. They do not allow outsiders to run nodes and instead operate jointly with a handful of selected partners. The advantage of consortium chains is that transfers can be extremely fast, gas fees can be eliminated altogether, and transactions can be fully aligned with regulatory requirements. Most people would never equate a consortium chain with a public blockchain, because the two are fundamentally different in nature.

So why did Tether and Circle choose this moment to launch consortium chains? The main reason is the same as why companies built intranets back in the day—to solve an urgent, short-term problem.

After the U.S. passed its stablecoin legislation 1, everyone wanted to enter the stablecoin business. But the upgrade pace of public blockchains—including Ethereum—couldn’t keep up with the surging demand. Financial institutions were saying: “I want to test stablecoin transfers tomorrow. How can I wait six months for Ethereum’s next upgrade?” This forced the two companies to come up with an immediate solution to satisfy client needs.

Money was already knocking at the door, but the infrastructure wasn’t ready. Suddenly, issues that few had cared about before—gas fee fluctuations, settlement speed, even transaction privacy—became urgent problems that stablecoin issuers had to fix right away. While the stablecoin business is lucrative, issuers don’t have secret breakthroughs up their sleeves. At moments like this, the CTO naturally tells the CEO: “The shortcut is to spin up our own consortium chain first, grab the immediate profits, and worry about the rest later.”

Of course, marketing wouldn’t present it this bluntly. Framing it as “ecosystem vertical integration” makes it sound more visionary, and even squeezes out extra profits. This reversed logic might fool investors, but it doesn’t explain why, if these problems are truly so critical, they are only being addressed now.

I believe Tether and Circle know very well that public blockchains are the only long-term solution. Both companies emphasize Ethereum ecosystem compatibility (EVM-compatible) on their websites and have never suggested replacing Ethereum or any other public blockchain. History is right in front of us. On top of that, the average gas fee on Ethereum L2s is already less than NT$0.01 per transaction. Even if it rose tenfold, the cost would still be unimaginably cheaper than traditional cross-border remittances.

To rationalize their blockchains, Tether and Circle have no choice but to blow small issues out of proportion. Ethereum, by contrast, positions itself as the World Ledger. In a recent interview, Vitalik Buterin said that Ethereum’s vision is focused on the next decade, with the goal of building a permissionless global settlement layer that can gradually support applications in social, gaming, finance, and beyond. He would rather tolerate short-term bottlenecks in scalability and privacy than take shortcuts that compromise Ethereum’s long-term decentralization, trustworthiness, and neutrality. That’s the difference between Ethereum and stablecoin issuers—and the key distinction between building infrastructureand launching products.

Short-Term vs. Long-Term

So what impact do Tether and Circle’s consortium chains have on Ethereum?

In the short term, the narrative of ETH appreciation may take a hit. Consortium chains purpose-built for stablecoins are like the old internet cafés dedicated to LAN gaming. For users who only care about smooth transactions, of course they’re more attractive. Many transactions that would have happened on Ethereum’s mainnet may instead be drawn onto these consortium chains. This is exactly what people worry about when they talk about “value leakage.”

But in the long run, history has already provided the answer: the greatest rival of internet cafés wasn’t other cafés, but broadband internet in every household. By the same logic, the challenger to Tether’s chain isn’t Circle’s chain—it’s general-purpose public infrastructure like Ethereum.

As consortium chains grow, their fundamental limitations will start to surface. What happens when a Circle user wants to swap USDC for an asset on Tether’s chain? Or when a Stripe merchant wants to settle with a supplier on another consortium chain? Since Circle and Tether are business competitors, they’re unlikely to build bridges for each other. At that point, what’s needed is a neutral public blockchain, belonging to no single company, to handle value exchange. That’s the role Ethereum plays.

That’s why I would argue the rise of these consortium chains doesn’t weaken Ethereum—it highlights its core value: credible neutrality. Ethereum’s narrative is indeed evolving. In the future, it may not be that all transactions happen on a public blockchain, but rather that Ethereum serves as the hub connecting various stablecoin consortium chains. The more consortium chains there are, the greater the demand for interoperability, and the deeper the reliance on Ethereum as the neutral “Internet.” Local networks never replaced the Internet. Unless Wall Street has learned nothing from that history, why else would institutions keep buying ETH even after Tether and Circle announced their blockchains?

1 The U.S. Passes the Stablecoin Act! Why Skip a CBDC and Still Come Out Ahead?